Whether you’re moving down the hall or across the country, using a change of address checklist to notify people of your whereabouts ensures important things like checks, statements, and notices don’t go missing.

There are so many people, companies, and institutions that need our addresses that it can be difficult to keep track of them all, so we’ve created a comprehensive list of where to change your address when you move. There are links to make things easier and highlighted organizations to prioritize. You’ll even find a printable change of address checklist, so you can keep track of updates you have left to do. By organizing your move efficiently, everything from bills to birthday cards will seamlessly follow you to your new digs.

When Do I Need to Change My Address?

Start letting businesses know about your relocation around 4 weeks before you move — it’s one of the key tasks on your moving checklist. Some places need to know sooner than others, especially when it comes to financial or legal reasons:

- Homeowners/Renters insurance policy: Whether you rent or own, let your insurance provider know of your new address and moving date. They can adjust your policy for your next residence and ensure seamless coverage.

- Utilities and internet: Make sure you have heat, hot water, and internet at your new location on moving day. Close your old accounts so you’re no longer responsible for bills at your former address.

- U.S. Postal Service: Arrange for the USPS to forward your mail so nothing falls through the cracks during your transition.

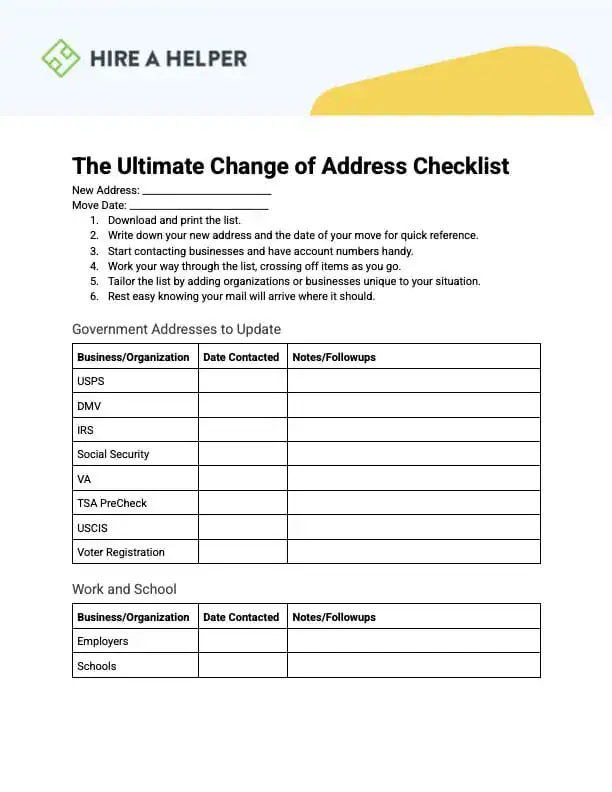

The Ultimate Checklist of Where to Change Your Address

Our downloadable checklist covers all the places you need to change your address and guides you through the process. Here are the steps to take:

- Download and print the list.

- Write down your new address and the date of your move for quick reference.

- Start contacting businesses and have account numbers handy.

- Work your way through the list, crossing off items as you go.

- Tailor the list by adding organizations or businesses unique to your situation.

- Rest easy knowing your mail will arrive where it should.

Mail Forwarding

USPS

At least 2 weeks before you move, submit a change of address form with USPS to reroute your mail. Most mail is forwarded for free, but there may be a fee for parcels like Media Mail. Standard mail forwarding lasts for one year and can be extended up to 18 months.

Government Agencies

Department of Motor Vehicles (DMV)

Most states require you to update your address with your local DMV within a certain period of time after moving. Change your address on your driver’s license and vehicle registrations. You can do these updates online or book an in-person appointment.

(info above from usa.gov)

Internal Revenue Service (IRS)

While you can notify the IRS of your new address when you submit your tax return, it’s best to update your account as soon as possible so you don’t miss refunds, notices, and important documents. You can do this in person, by phone, by letter, and by submitting Form 8822.

Social Security Administration (SSA)

If you receive retirement, disability, Medicare, and other benefits, update your contact information with the SSA. Even if your benefits are direct deposited, the government needs your correct mailing address on file.

Veteran Affairs (VA)

Whether you’re a veteran, service member, or family member, log into your VA account online to change your contact information. This ensures correspondence related to benefits, medical care, and loans gets to you promptly.

TSA PreCheck and Trusted Traveler Programs

The government needs your current address for identification verification if you have travel privileges through TSA PreCheck and Trusted Traveler.

- For TSA PreCheck, contact the enrollment provider you applied with.

- For Global Entry, NEXUS, SENTRI, or FAST, sign in to your Trusted Traveler Program account.

U.S. Citizenship and Immigration Services (USCIS)

Update your address in your USCIS account to receive documents related to green cards, work permits, citizenship, and other immigration benefits. Depending on your status, you may be required to notify USCIS within 10 days of moving.

Voter registration

In some states, the DMV can update your voter registration when you change your driver’s license information. Otherwise, the National Association of Secretaries of State can connect you to your state election office.

Work and School

Employers

Your boss needs a heads-up about your new address for tax and payroll forms. Some employers also base salary and benefits on location. Contact your HR department as soon as you’re able so they can get the process started for you.

Educational institutions

Don’t miss tuition bills, financial aid notices, transcripts, report cards, and certificates. Whether you’re studying full-time or part-time, or your kids are in school, each institution needs your current address to send important documents.

“…You must update your address with every organization separately. USPS only reroutes mail sent to your old address. It doesn’t make address changes for you.”

Keep in mind that your change of address might come with a change in school district, so be sure to keep track of all the paperwork involved in that as well.

Household Utilities and Services

Electricity, water, and gas

If you’re still within the same service area, you can transfer utility accounts to your new address. Otherwise, close your accounts and arrange for services to begin at your new address. There are sites that use your zip code to tell you what utilities are available near you.

Voice, internet, and cable

Many cable, phone, and internet providers have processes to help you change your address on your account and transfer service. Below are links to a few of the larger providers.

Miscellaneous utilities

Depending on where you live, you might be billed separately for sewer, recycling, or trash. Don’t forget to change your address with these companies and cancel service if you’re moving to an area where they don’t operate.

Financial & Legal

Banks

Even if you bank online or receive e-statements, certain communications (or checks!) may be sent by snail mail. Make a list of, and follow up with, institutions where you have:

- Checking and savings accounts

- Safety deposit boxes

- Investment portfolios

- Lines of credit

Credit cards

Credit card companies also need to learn of your new address. Pull out all the plastic in your wallet and call the customer service number on the back of each card. You can also log into each card’s online portal or app and update your address there.

Lenders

If you have any type of loan, including mortgages, car loans, and student loans, change your address with the lenders so you can receive important information and updates.

Investment accounts

Think about investments that you have tucked away, and contact brokerage or investment companies you have accounts with. You’ll want a reliable way to receive statements and tax forms aside from email.

Insurance providers

Follow up with companies where you hold house, car, health, and life insurance. Forgetting to update a policy could cause it to lapse, especially if the insurance is related to your residence. Speak with someone directly to ensure your coverage stays active.

Digital payment platforms

Mobile apps like PayPal, Venmo, Apple Pay, Google Pay, and Zelle may use your address to verify your details and provide tax information. Log into your profile on each payment app to ensure your details are accurate.

Financial and legal consultants

Your financial planner, accountant, attorney, estate planner, and other professionals should also be on your change of address checklist. Run through your contact list and send quick e-mails to your advisors so they can update their records and share important documents.

Health and Wellness

Health care providers

Include your health care providers on your list of addresses to change when moving to receive bills, reminders, and notices. Reach out to your:

- Doctor

- Dentist or orthodontist

- Optometrist

- Physiotherapist

- Naturopath

Pharmacy

Whether you pick up prescriptions in person or have them delivered, your pharmacy needs current information. Give them a call to update your address or transfer prescriptions to a pharmacist closer to your new home.

Veterinarian

Don’t forget about your furry friends! Give your vet clinic your new address and update your pet’s microchip registry in case your animal goes missing. If you use traditional collar tags for more than your pet’s name, make sure the contact information on the engraving is correct.

Memberships and Subscriptions

Newspapers and magazines

Whether you like to read about fashion or finance, you’ll want your favorite newspaper or magazine to land on your doorstep after a move. Updating your subscription information online ensures you don’t miss an issue.

Institutions and associations

Give your new address to any organization that you’re involved with. These can include:

- Places of worship

- Professional memberships and networking groups

- Licensing boards or credentialing bodies

- AAA

- AARP

- Alumni groups

- Charities

- Children’s clubs

- Civic clubs

- Country or social club

- Neighborhood association

- PTA

- Political parties

Shopping and Services

Warehouse clubs

Costco, Sam’s Club, and membership-based retailers need your address to send rebates, coupons, renewal notices, and online orders.

“Start letting businesses know about your relocation around 4 weeks before you move…some places need to know sooner than others, especially when it comes to financial or legal reasons.”

Stop by the membership desk next time you’re in the store or log into your account to make changes.

Online retailers

Many online retailers store your address to make it easier for you to check out. The next time you use sites like Amazon or Walmart, change your shipping information so your order goes to the right place.

Loyalty programs

If you collect points for air travel, hotels, groceries, or other purchases, let the company know your whereabouts so you can receive membership cards and offers, and claim your rewards.

Subscription boxes

If your Hello Fresh, BarkBox, or similar deliveries go to the wrong house, that’s cool for the new residents, but not so much for you. Double-check that your new home is still within their delivery areas and update your address so your curated goodies make it to your new home.

Auto-ship items

Regular shipments of toilet paper, vitamins, laundry soap, coffee, and pet food keep your household running smoothly — but only as long as they show up in time. Change your address for any auto-shipping purchases. You might also pause them until after your move to simplify packing.

Streaming platforms

Even though digital streaming services don’t send mail, they need your current billing address to process payments. Keep your account information updated on platforms like Netflix, Hulu, Spotify, and Apple Music so they don’t stop working in the middle of your binge.

Home care

Do you have regularly scheduled visits from cleaners, pest control, landscapers, pool maintenance services, or snow removal companies? Book your last appointment at your old place and arrange service at your new home if needed.

Family and Friends

Sometimes, surprises arrive on your doorstep: birth announcements, wedding invitations, care packages, and flowers. Email your new address to family and friends (or send a message in your group chat) to stay connected.

FAQs

If I change my address with USPS, do I still need to let each of these places know I’m moving?

Yes, you must update your address with every organization separately. USPS only reroutes mail sent to your old address. It doesn’t make address changes for you.

When do I need to change my address when I move?

Start notifying people of your new address about 4 weeks before you move. Prioritize the USPS, insurance, utilities, banks, and government on your change of address checklist. Less urgent accounts can be updated closer to or after your move.

What happens if I forget to update my address when I move?

Set up mail forwarding by USPS to ensure nothing is lost. Each time you receive a forwarded piece of mail, add the sender to your change-of-address checklist, so you’ll know who still needs your new address.