The number of U.S. citizens moving to Mexico in 2022 is set to reach 18,161 — the highest in nearly a decade

More than half (52%) of Americans who moved to Mexico in 2022 were retirees

Jalisco and Mexico City attract nearly a third (31%) of all U.S. citizens moving to Mexico

Rent is two times lower than in the United States, on average

There was an avg. of 1,870 monthly Google searches for “moving to Mexico” in 2022 — a 42% YoY increase

North Carolina (+75%), Texas (+65%), and Florida (+60%) saw the greatest YoY increases in Google searches for “moving to Mexico”

The number of Americans moving to Mexico over recent years is estimated to be between 800,000 and 1.5 million. And lately, that number has been growing rapidly.

But what is the cost to the country? The influx of immigrants with higher incomes is reportedly having adverse effects on the local population; there are reports of gentrification in Mexico City, rents doubling in Tijuana, and foreign demand driving up prices in Quintana Roo and Baja California Sur — all places that are among the top destinations for Americans settling into Mexico.

Let’s dive into the numbers and see just how many Americans have moved to Mexico in 2022.

Going South: Migration to Mexico To Reach New Heights in 2022

As reported in our recentstudy of Americans moving abroad, 10,594 U.S. citizens have taken residence in Mexico so far in 2022.

Not only is that 22% higher than by the same time last year, but at this rate, it’s estimated18,161 Americans will have moved to Mexico by the end of 2022. That figure is higher than in any year since 2013.

When looking at this trend in more detail, the number of temporary residents (as opposed to permanent residents) has increased sharply. Temporary residents are defined as people who intend to stay in Mexico forlonger than 180 days for the stated purposes of either work, study, reunification with family or business ventures.

“… it’s estimated 18,161 Americans will have moved to Mexico by the end of 2022. That figure is higher than in any year since 2013.”

Already in 2021, over 9,000 U.S. citizens have successfully applied for a temporary residency in Mexico; that’s the highest number of applications over the last decade!

By the end of this year, Mexico is on track to receive 10,780 Americans as new temporary residents.

Jalisco — Not Mexico City — Is the Top Destination for American Immigrants

There is certainly a lot of buzz about Americans moving to Mexico City, but it is the state of Jalisco that consistently sees more U.S. citizens moving in than Mexico’s capital… or any other state for that matter.

Over 2,000 Americans have moved to Jalisco in 2022, and that figure is likely to reach 3,400 people by year’s end. That would mean nearly one in five (19%) Americans moving to Mexico choose to move to Jalisco, a West Coast city.

The nation’s capital, Mexico City, isn’t too far behind Jalisco. Mexico City has seen 1,315 American move-ins so far in 2022, with 2,254 projected by year’s end (~12% of the total migration). Baja California Sur also ranks high, with an estimated 1,867 new residents from the United States, (~10% of the total inflow).

Another state that seems to be fast becoming a popular destination is Quintana Roo.

Best known for being home to Cancun, this state is beginning to attract Americans looking to live (and not just party) there. In 2022, Quintana Roo is projected to attract nearly 13% of all moves from the United States — that’s second only to Jalisco.

Taken together, these four states receive the majority (54%) of all Americans moving to Mexico.

Moving far away?

Do it cheaper.

MovingPlace can save up to 40% compared to traditional interstate moving companies. Click here to learn how.

Remote Work? More Like Retirement! Most Common Reasons for American Immigration to Mexico

Since 2012, almost a third (31%) of all Americans who moved to Mexico as temporary or permanent residents reportedly did so for work. That’s based on the official immigration statistics which group all new residents into categories of “work”, “family reunification”, “retirement”, and “other”.

An additional 23% of immigrants from the United States get their resident permits in Mexico by being a family member of either a Mexican national or another U.S. citizen who already has a valid residence permit.

The most popular category of permits issued to Americans is called “rentista” – which is the most common route to residency for retirees.

In the last decade, 40% of all U.S. citizens who took up residency in Mexico were retirees; this year, that share has jumped to 52%. In other words, over half of all Americans moving to Mexico are reportedly doing so during their retirement. This might suggest U.S. cost of living is having an impact on social security stability as well.

Tourists or Residents?

And what about that segment of American remote workers whose moves to Mexico have been subject to much discussion and debate?

As the number of U.S. citizens moving to Mexico is setting new records, in some parts of Mexico, calls for Americans to go back home are beginning to be heard.

While Mexico does offer a Temporary Resident Visa for remote workers under the Financial Solvency clause, official statistics don’t distinguish these types of residents from other temporary resident holders. It is likely that they are bundled into the “Other” category, which also covers people relocating for scientific research, government work and more.

Iit’s reasonable to assume remote workers who are giving Mexico a goare likely making use of Mexico’s easy-to-obtain tourist visas, which allow immigrants to stay in the country for up to six months.

Summer Spike: Searches for Moving to Mexico Peaked in June 2022

The data show no sign of American immigration slowing down anytime soon. On top of the growing number of recorded moves, moving intent (signified by Google searches for “moving to Mexico”) is the highest it’s been in years.

“…there wasn’t a single state that didn’t increase their Googling of Mexico.”

From 2019 to 2021, the number of monthly Google searches for “moving to Mexico” tended to stay between 1,500 and 2,000.

By the middle of 2022, however, these searches reached 3,100. Though it’s not simple to know the causation, that spike correlates with the U.S. Supreme Court’s overturn of the precedent-setting Roe v. Wade decision, as well as 9.1% currency inflation in America — its highest rate in 40 years.

Where in America ‘Moving to Mexico’ Searches Peaked

The average number of monthly Google searches in America for “moving to Mexico” rose roughly 36% year-over-year, reaching 2,100 searches in 2022 — that’s up an average of 1,550 searches.

Overall, there wasn’t a single state that didn’t increase their Googling of Mexico; all states saw greater search volume for “moving to Mexico” this year as compared to 2021.

Some states, however, stand out. In North Carolina, there was a 75% increase in Google searches for “moving to Mexico”. Searches also jumped 65% in Texas and 60% in Florida, respectively.

By contrast, California, where the number of “moving to Mexico” searches is the highest in the country, only saw a Google search increase of 15% in 2022, as compared to last year.

Moving far away?

See prices for container labor – instantly.

Read honest customer reviews.

Book everything online.

All About Affordability: Why Mexico Attracts Expats From Around the World

Mexico is finding itself to be a magnet not only for Americans, but for expats across the globe.

In its Expat Insider 2022 report, Inter Nations — an expat community hub — named Mexico the number one country for expats. Among the aspects that propelled it to the top spot are “affordability” and “ease of settling in”, which both listed Mexico as the very best in the world.

“It’s reasonable to assume remote workers who are giving Mexico a go are likely making use of Mexico’s easy-to-obtain tourist visas, which allow immigrants to stay in the country for up to six months.”

Affordability of housing and medical care are also likely to attract Americans; both are increasingly unaffordable for vast strands of the U.S. population.

Healthcare

A survey commissioned by ExpatsInMexico – an online magazine for foreigners living in Mexico – found that for 75% of expats, $150 per month covers all of their healthcare needs. It’s an attractive proposition for retirees, who make up 80% of the survey respondents and are likely to spend twice that amount, at minimum, if they remained in the United States.

Rent

Rent is another big immigration factor. When in the United States, the average rent is now over $2,000, and growing in over 90% of U.S. cities, the average rent in the four states of Mexico that are top destinations for U.S. immigrants is below $800.

Of the four top destination states, rent is lowest in Jalisco ($720 per month) and Quintana Roo ($735). Rent is slightly higher in Mexico City ($787), and noticeably higher in Baja California Sur ($925). (All figures are expressed in average dollar amount after conversion.)

Sure enough, the houses and apartments Americans moving to are likely to be at the higher end of the price spectrum. But if you consider that most Americans moving to Mexico are retirees, rents this low must be extremely appealing, even if they sold their homes to make the move.

Sources and Methodology

Official immigration statistics come from the Unidad de Política Migratoria – Boletines Estadísticos and were used to estimate the number of Americans moving to Mexico. Only moves requiring either a temporary or a permanent work permit were counted. Military moves were excluded, as were the moves for temporary purposes, such as business and tourism.

The total and average monthly search volumes for the keyword “moving to Mexico” were taken from Google Ads API.

Rent prices for Mexican cities were sourced from Propiedades.com, while the estimates of average rents in the U.S. were taken from Redfin.

With Valentine’s Day and the scent of relationship milestones heavy in the air, it’s time to talk about one of the biggest milestones of all: moving in with a romantic partner.

If you’re considering moving in together, my assumption is that you’re already bringing all the love and excitement and ooey-gooey feelings to the situation — which means that it’s my job to bring the practicality, organization, and the cold hard sense. This wretched Virgo thrives on sucking the joy out of situations, replacing it with a structure that will serve you well, far beyond your relationship’s honeymoon phase. (Spoiler alert: in my experience, all that good stuff comes flowing back in once you’ve set up a solid foundation.)

Here’s a list of some of the un-fun, straight-up, business-like details that have made living with a partner so much better for me.

Decide whether you’re clean-slating-it, or moving into one of your existing spaces

If one of you lives in a two-bedroom alone while the other lives in a lofty attic garret, this is probably a no-brainer. But in my experience, few situations are that simple.

I absolutely loved the studio I was living in when I met my boyfriend, and by the time we moved in together, I’d been living there for seven years. It was basically my longest relationship, outlasting all the boys I’d dated along the way, proving itself reliable in ways they hadn’t been.

Still, my initial thought was that I wanted to start somewhere new with my boyfriend; I wanted to live somewhere neither of us had a history with. Realistically, this was going to create more issues than it solved. For one, my boyfriend had just moved into his roomy one-bedroom a year before, at which point he’d paid a hefty broker’s fee. (This is a cute thing that used to be legal in New York City, and was the bane of our collective existences.)

“…(W)e each ended up saving $630 on rent by moving in together.”

The fact that it made more sense for me to move in with him was staring us in the face, so I asked him for a couple things to make that prospect more comfortable for me.

First, I wanted reassurance that I could bring my own decorating touch to the space, and secondly, I wanted my vote to count a bit more the next time we went apartment-hunting.

Since I hadn’t had any input in the selection of this current apartment, and it wasn’t a space I was super excited about, it felt only fair that I could weigh in extra on the next one! Happily, my boyfriend agreed. Something we’ve embraced in our relationship is that a compromise doesn’t have to just fall on one person; if there’s something you’re giving up, think about what you’d like to ask in return. Keep it within reason, of course, and don’t try to punish each other when you don’t get your way. But always ask for what you want — the worst your partner can say is no.

Don’t be shy about talking moving costs

We — or rather, I — now had a move to organize. Which was a particularly intimidating prospect after so much time in the same space. I’d been accumulating items around me like a cheerful little magpie for almost a decade, so there was a lot to dig through, get rid of, and sell-off.

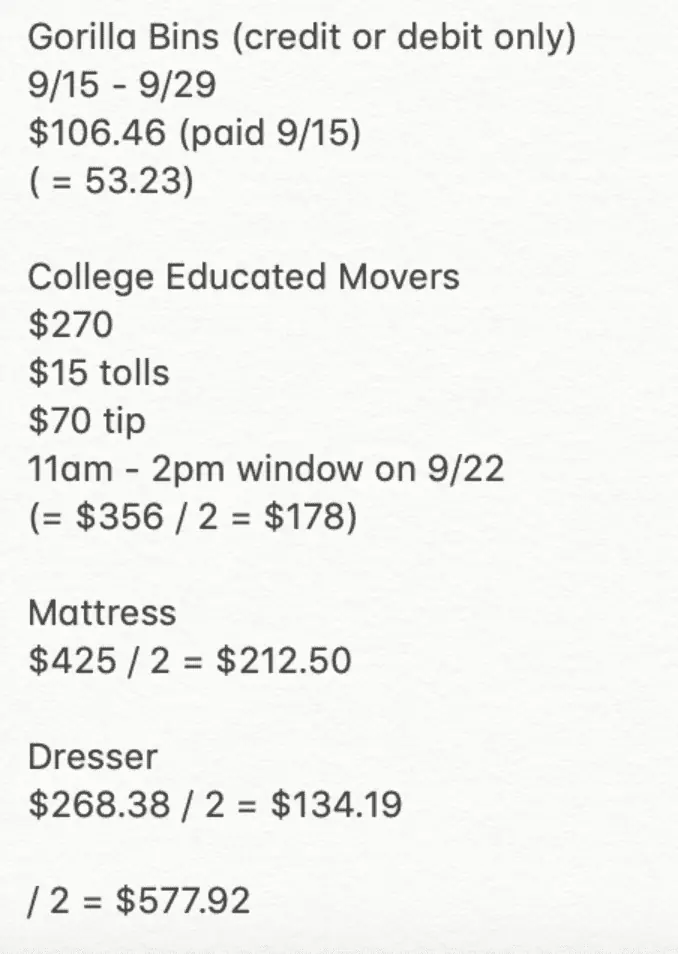

This was our actual moving cost list, which we decided to split.

I know my own space and I like things a certain way, so I was happy to take on the labor and organizational side of things. In exchange, my boyfriend offered to split the moving costs with me, which brought a whole range of new options within reach, like rental boxes from Gorilla Bins, and a team of local L.A. movers, which I’d never been able to spring for before.

Since he was getting to miss out on all the most annoying parts of moving, he reasoned, it only made sense that he could contribute to the process financially.

According to my moving spreadsheet (lol), we each paid $577.92, all told. This included the bins, the team, the tip and tolls for the truck, and a mattress and dresser we purchased for our shared space. It might sound high, but I was able to pay down my end by selling big-ticket furniture items that wouldn’t be making the move, and we each ended up saving $630 on rent by moving in together. The whole extravaganza more than paid for itself within just two months.

Get all math-y with how you split rent

Talking about money can be fraught for me, which I counter by talking about it pretty much all the time to build up my resistance. One area where I still struggle, though, is in asking others for money.

When we first moved in, my boyfriend was making about three times what I did. (Incredibly, data science pays slightly better than freelance writing and bartending.) But for my own reasons, I wasn’t comfortable asking him to pay two-thirds more rent than I was. If you are, that’s great! You should lean into that hard. But if you’re like me, I have a solution for you.

I suggested to my boyfriend that we come at the rent split from a different angle. Aside from the mushy romance stuff, a big part of wanting to move in together was a desire to save money, which is why we ultimately decided to base our rent split not off of what we were spending, but what we were saving.

With a standard split on our $1,750 Queens one-bedroom, my boyfriend would be saving $875 on what he used to pay, while I’d be saving just $385 on my old $1,260 studio. It was a great amount to be able to bank every month, but I was jealous of my boyfriend’s much larger savings.

“…(W)e ultimately decided to base our rent split not off of what we were spending, but what we were saving.”

To make the split more equitable, we added $875 and $385 together to get our total savings, then divided by two to find the average. The answer was $630, which we subtracted from each of our prior rents. I’d be paying $630, and he’d be paying $1,120. Not quite a two-thirds split, but one I never would’ve felt comfortable asking for without the power of math.

These days, the gap has closed between our incomes, so now we are able to do a true 50/50 split, but the above method served us well for over a year. I’d highly recommend it to anyone taking the leap to cohabitation.

See prices for movers by the hour – instantly.

Read real customer reviews.

Easily book your help online.

Make your lovely, wonderful significant other sign a dry, unromantic cohabitation agreement

As a child of separation and a graduate into the recession, my fundamental understanding of the world is that most things fall apart (cute!). But I’ve learned to speak my expectations so that others have a chance to respond calmly, or run screaming into the sea.

Coming into this glorified roommate situation after seven years of solitude, I figured I was probably bringing some pretty serious expectations to the table, so I asked my boyfriend if we could lay out a document spelling them out. Our agreement detailed the aforementioned rent split, what goes down if we break up, and what major responsibilities we’re each expecting from the other in the meantime.

Some things we considered:

Who buys groceries? Can we eat each other’s food?

Answer: we both buy groceries, but he buys more because I cook more. Any food is up for grabs, but there should be communication for specialty items that one of us has been looking forward to.

Does one of us like cleaning, or should we maybe spring for a monthly service?

Answer: one of us likes cleaning, and it’s me. I do it once a week, and if I need or want anything from my boyfriend, I let him know.

If we break up, can I have this couch please?

Answer: yes, because I’m the one who designed it and got us a discount on it.

Should we get a joint bank account for some of our expenses?

Answer: yes, at Simple and then Ally, but let’s keep the majority of our finances separate.

Can we please get renters insurance?

Answer: yes, an Allstate policy costing $13/month that we’ve transitioned to a USAA policy at $24/month.

Which streaming platforms do we want?

Answer: unfortunately, all of them. But we’ll cobble them together in a way that makes sure we’re each paying for our fair share.

What are your ideal bedtimes and wake up times?

Answer: I’m an 11p.m.-7a.m. “bb”, but he’s a 1a.m.-10p.m. angel, so we tried it his way for a while and have now settled on an 11:30p.m.-8:00a.m.-ish situation.

How much time do we each need alone?

Answer: we decided we each get a minimum of a couple hours a day separate, him to play video games or chat with his friends, and me to play my silly little iPhone games and watch my television stories.

How much time do we like to have together?

Answer: a lot, but there’s such a thing as too much, so let’s keep an eye on that.

Will Judge Judy be impressed with us if she ever reads this?

Answer: nothing impresses her, but also yes.

Not every item made the final list, but putting it together gave us each an opportunity to share our biggest needs, wants, and fears about combining our lives, and it ended up being an incredibly productive conversation — one that we revisit every August to make sure we’re both still comfortable and feeling good.

And that feels like a good thing to add here: we are still a couple, and living together quite happily — in a Los Angeles apartment that I got a big vote in picking out — paperwork, uncomfortable conversations and all. We not only like and love each other, but respect each other’s boundaries, which gives me true confidence in the longevity of this match!

My partner is Chinese-American, so ideally he and I would like to put down roots in a city with a not insignificant Asian-American and Pacific Islander (AAPI) population. (This rules out cities that might have made my list back when it was just me, my white self, and I.)

In the past, we’ve lived—both separately and together—in diverse places like Boston, New York, Los Angeles, Rockville, Maryland, and Portland, Oregon. Yet ultimately, we want to live in a city that currently has an Asian population significantly higher than the national average, which hovers right around 7%, according to Pew Research Center.

The reasoning of course is for both comfort and safety reasons. But while we want a piece of that suburban pie, we’d also like to give ourselves a liiiittle bit of distance from big city life. (Ideally, we’d live just far away enough that we can watch House Hunters without stewing in shame over the amount we pay to live on the square footage of a postage stamp.)

But what is anyone’s option for a more suburban and affordable lifestyle within a city or town that isn’t exclusively white? I’m so very glad you asked, since we’re sharing all the research we did for ourselves.

Our search for an Asian community as an interracial couple

Really quickly before I dive in, I want to note a couple things.

First of all, I’ll be citing two statistics for each location: the “Asian alone” population percentage from the United States Census Bureau, which includes solely those responders who are “reporting only one race”. For living purposes, I’m also citing the median gross rent for 2015-2019, a representation of what a middle-of-the-bell-curve citizen pays every month in rent and utilities. (Basically, this is an all-inclusive housing cost, which for your reference is $1,664 in West Hollywood—a number that’s lower than our outright rent… so I guess take these with a grain of salt?)

“…we want to live in a city that currently has an Asian population significantly higher than the national average, which hovers right around 7%, according to Pew Research Center.”

I point out that first statistic to underline that these aren’t necessarily the most diverse cities overall, as we’re seeking solely the percentage of Asian populations for our particular situation.

Honolulu, Hawaii

Median Gross Rent: $1,745

A big part of my brain doesn’t think I’m allowed to live in a place like Hawaii, because it feels like a reward I haven’t earned. But if I can get past the mental block of whether or not I deserve to live and work on a tropical island, it actually seems like a great setup. In a reversal from every other city on this list, Caucasians are in the minority in Honolulu—people of solely Asian descent represent 42.9% of the population, as compared to 17.9% white people. And that doesn’t even include native Hawaiians or Pacific Islanders (9.6%), or those who represent multiple races (22.8%), which boosts the numbers even higher.

Seattle, Washington

Median Gross Rent: $1,614

Across the pond and nestled snuggly into my beloved Pacific Northwest, we have chilly little Seattle, one of the few cities on this list that my partner and I have visited together. We stayed in a pretty industrial area during our visit, which neither of us was super keen on, but I’m still thinking about our day trip out to Bainbridge Island. I’m betting there’s a neighborhood that would check all our boxes.

At the end of the day, it’s hard to argue with the gorgeous views, fresh seafood, and younger-skewing demographics—plus it hits our checkboxes with an Asian-American population of 15.4%.

Get Help Unloading Your Rental Truck

See prices for movers by the hour—instantly.

Read real customer reviews.

Easily book your help online.

Portland, Oregon

Median Gross Rent: $1,248

Sooner or later, they all come crawling back. (At least, according to my social media-stalking of my former high school classmates.) I’ve so far resisted making the full move back to my hometown, but it always shimmers on the horizon. And now that I’m back on the same coast, it feels like just a matter of time. This is especially due to the fact that while Portland has a genuinely terrible record in terms of a lot of diversity, it does host a not-too-shabby Asian population at 8.2%, so it’s worth considering for us. Rents seem great at the moment, but once we’re looking to buy property, we’d probably steer clear of the Portland housing market for a few years, because it is going absolutely bananas right now.

San Diego, California

Median Gross Rent: $1,695

There are quite a few cities in California that match our requirements, but since I didn’t want to pull more than one option from any given state, the best choice is definitely San Diego. My partner and I visited earlier this year, and all I kept saying was, “Los Angeles wishes!” Same gorgeous weather as LA, same basic lifestyle vibe, similar diversity (with 16.9% Asian population), but cheaper, less sprawling, and way more laid back. (Sorry, LA, but you are a bit of a try-hard in the coolness department.)

Chicago, Illinois

Median Gross Rent: $823

Continuing our jaunt eastward, we have to leapfrog a few particularly homogenous states before landing in the lovely little enclave that is Chicago. This is another city that I visited and just had an absolute blast in, although I’ll note that it was in summer, and I’m told that to really get a feel for it, I need to try my hand at Chicago in the winter. But I adored the energy. I found the public transportation system super intuitive, and I simply love to see a median gross rent in the triple-digits.

And while the Asian population currently registers at 6.6%, the midwest is currently home to the fastest-growing Asian American communities, so I’m betting that number will rise. Plus, my partner and I both do long-form improv (humiliating), so Chicago would be an excellent place to keep our comedic skills sharp.

Austin, Texas

Median Gross Rent: $1,280

I gotta be honest, I initially thought the majority of the South would probably be out, but Texas went and surprised me! I’ve not had the pleasure of visiting the state in the past, but I always toyed with the idea of moving to Austin, which I’ve been told has similar vibes to Portland. With an Asian population of 7.6%, it’s just above the national average. But the fact that there’s a significant Latinx community (33.9%) is a nice boost to our search. So Barton Springs, here we (maybe) come!

Newton, Massachusetts

Median Gross Rent: $1,940

After a decade in New York City, I’m a little hesitant to settle in a nearby city like Boston. I scooted next door to Newton to check out the scene and am very happy with what I found.

Once again, it’s close enough to the city that we wouldn’t have to quit urban sprawl cold turkey, but could instead take it in manageable doses. Plus, Newton actually has a significantly larger Asian population—14.8% compared with Boston’s 9.7%—along with great public schools, a suburban feel with great parks, coffee shops, restaurants and multiple awards for being one of the nicest places to live in the United States. (One con? It also has the prices to go with all those pluses.)

Rockville, Maryland

Median Gross Rent: $1,921

Alright, if my hometown can be on this list, so can his. Not only does Rockville boast a double-digit Asian population at 21.1%, but it’s truly a suburban dream. Rockville is both close enough to DC that it’s not a total nightmare to get to, but secluded enough that I can sleep through the night without getting jolted awake by car alarms or helicopters like we do in LA. Plus, my partner still has a tightly-knit community of friends out there that would be amazing to live nearby.

Philadelphia, Pennsylvania

Median Gross Rent: $1,042

Once again, Philly is just a sliver above the national average at 7.2%, but I’m leaving Philadelphia on the list because I’m intrigued, okay?

Personally, I visited the city once, back in college, and found it very approachable with locals who are very direct, which is a personality type I absolutely love. Plus, I feel like I can’t stop reading headlines about what a great place it is to live, with excellent historical and cultural institutions, and an impressive confluence of affordable housing and job growth.

Fort Lee, New Jersey

Median Gross Rent: $1,923

Does it feel absolutely counterintuitive for me to move all the way back to within eyeshot of New York City without actually moving into the city itself? Yes, yes it does, which is why Fort Lee is at the very end of the list. But it has an Asian population of 42.5%, which is exactly what we’re looking for!

But for me, I’ve already lived at one end of the George Washington Bridge and had about as great an experience as I’d imagine I could, living in a well-priced Manhattan studio for seven glorious years. Trying my hand at a life on the opposite side of the bridge feels like it would only invite—and suffer from—comparison. But truly, all the blessings in the world to everyone who does live there now.

Final protip

Those are the cities we have so far, but to add to the list, my partner had an excellent suggestion that you could potentially use as well: search H-Mart locations. (If a city has an H-Mart, you should consider moving there regardless, because it’s an incredible store.)

If you’re searching for “asian communities near me”, this can also tell you that the area has the population to support this kind of store, and is a great indicator for pockets of diversity that might not necessarily show up in the cold hard stats I’m relying on here.

In 1970, the median age of first-time homebuyers was 30.6 years. Today, according to MarketWatch, the median age of American homebuyers is 47 years. Since the 2007-2008 financial crisis alone, the median age has increased by eight years, and that rise is largely attributed to the dramatic decrease of millennials entering the housing market.

The American Dream is changing, and with it, the fundamental desire to own a home.

In 2019, only 43% of millennials owned the homes they lived in, compared to 66% of generation X and 77% of baby boomers. A combination of debt, high housing costs, and a generation with different priorities all contribute to millennials forgoing homeownership.

An important policy goal of the US government has long been to encourage homeownership. Historically, that’s been done through the federal tax code and residential mortgage regulation. But since these things benefit mostly higher-income, better-educated homeowners, these policies are no longer as effective as they once were.

The Brookings Institute points out that a better path to encouraging homeownership at a younger age would be implementing policies that create more opportunities for wealth-building. But until that happens, the median age is likely to keep increasing.

Here are the biggest factors contributing to the wealth gap.

Student loan debt

Student loan debt plays a massive role in millennials deciding not to buy a home. In a survey of student loan borrowers, 83% of non-homeowners cite student loan debt as the reason they haven’t bought a house. Indeed, the average monthly student loan payment is $393 a month, which leaves many unable to save for a down payment on a home.

The most recent student loan debt statistics show that in 2020, there were almost 45 million student loan borrowers who had an average debt of around $33,000.

Rent burden

Millennials are more rent-burdened than any other generation. Rent burden occurs if more than 30% of your income goes toward paying rent — and millennials spend 45% of their income on rent. And while the average living wage is $68,808 a year, the average millennial makes just $35,592 a year, and rent burden plus low wages create a double-whammy for many young people.

“Whether or not you can afford to buy a home depends on your income, the property prices in your location, how much other debt you have, and how good your credit score is.”

Delayed marriage

Marriage increases the chances of homeownership by 18%, and according to the Urban Institute, delayed marriage is one of the biggest factors for why millennials aren’t buying homes. In 1960, couples typically entered their first marriage in their early 20s, but today, the median age for a first marriage is nearly 30.

Delayed procreation

Having children is another important factor in people’s decision to buy a house — having kids increases a person’s chance of homeownership by 6%. But millennials are in no big hurry to have kids. In 1990, 37% of married couples aged 18 to 34 had children, but in 2015, just 25% of young couples were parents.

More diversity, more inequities

The millennial generation is far more diverse than previous ones. According to the Brookings Institute, the young adult age group was 73% white in 1990. In 2000, it was 63% white. Today, the millennial generation is around 56% white, with 30% of its population made up of Hispanics, Asians, and people who identify as two or more races. Historically, homeownership rates are lower among Black, Hispanic, and Asian Americans when compared with white Americans — and today, just 14.5% of Black millennials own a home, compared with 39% of their white counterparts.

What Does it Realistically Take to Buy a House or Condo?

Maybe you’re not interested in becoming a homeowner at a tender age, and that’s perfectly fine. Renting definitely has advantages over buying, and if you prefer the unencumbered life, apartment living frees you up to move wherever, whenever.

However, if you dream of homeownership — but feel like it’s only a pipe dream — you might want to look into homeowner rates to be sure. In many cases, a mortgage is less expensive than rent, and a number of federal and state programs exist solely to help first-time homebuyers like yourself. You might be surprised to find you can afford to buy a home, after all.

You have to use the “28/36 Rule”

Whether or not you can afford to buy a home depends on your income, the property prices in your location, how much other debt you have, and how good your credit score is.

A good starting point for figuring out whether you can afford to buy a house is to use the “28/36 rule”. This rule states that your total household expenses (including your mortgage, utilities, and property taxes) shouldn’t exceed more than 28% of your gross monthly income, and your total household debt (like credit cards and car loans) shouldn’t be more than 36% of your gross monthly income. So figure out those percentages, and you’ll have a rough idea of what you’re working with.

The lowdown on home loans: How do mortgages work?

Unless you’re loaded with cash, you’ll need to get a mortgage like most people. But what specifically is a mortgage, anyway?

A mortgage is an agreement between you and a lender (typically a bank but not necessarily) that says the lender will give you money to buy a house, but if you don’t make the monthly loan payments, they’ll take it away, and you’ll lose any equity (ownership) you’ve built up. A mortgage payment is like rent, but for homeowners. When you borrow money to purchase your home, you pay it back over, say, 15 or 30 years, with interest. The bank figures out how much this adds up to each month, and that’s your mortgage payment. Once your mortgage is paid off, you have full ownership of your home.

What’s the deal with interest rates?

Interest rates are calculated as a percentage of your mortgage loan. Each mortgage payment you make pays back a portion of the principal (the full amount you borrowed) plus the interest that accrued that month.

Fixed-rate interest means that your interest rate won’t change during the life of the loan, and you’ll pay back the same amount each month.

Adjustable-rate interest means that the interest rate may change under certain conditions, and if it does, your lender will adjust your monthly payments up or down until the next rate change.

The longer you take to pay off your mortgage, the more you’ll end up paying in interest. The best way to keep your interest rate low is to pay back the loan as soon as possible, never forget a payment, and pay more than your monthly minimum, if possible.

What Are ALL the Costs Involved in Buying and Owning a Home?

Here is a list of important terms to learn and keep handy, even if you know them backward and forwards.

Down payment

Traditionally, people buying a home pay 20% of the price of the house up-front. It’s possible to buy a home with a smaller down payment, although that could mean increased borrowing costs and higher monthly payments.

Closing costs

Closing costs are lender and 3rd party fees and expenses that are paid at the close of the sale transaction. These costs run roughly 2-5% of the loan amount and could include things like appraisals, taxes, insurance, prepaid interest, and application, origination, and attorney’s fees.

Some lenders allow you to fold the closing costs into the loan, but that makes your loan payment higher, and you’ll end up paying interest on those costs for the life of the mortgage! Your lender will outline your closing costs in a Loan Estimate, which you’ll receive when you apply for the loan.

Monthly mortgage

Your monthly mortgage payment depends on the amount of the loan + your interest rate.

Property taxes

The Man’s gotta take his chunk, and property taxes is how it’s done. Your property taxes pay for things that make your community better, like schools and road repairs. Property taxes are based on the value of your home, and rates vary by location and fluctuate often due to changing needs and priorities in the community.

“In 2019, only 43% of millennials owned the homes they lived in, compared to 66% of generation X and 77% of baby boomers.”

Homeowner’s insurance

Homeowner’s insurance covers losses and damages to your house and assets due to theft or damage. Rates vary by state and region, but the average annual premium in 2017 was about $1,200.

Hazard insurance

Hazard insurance is a more extreme homeowner’s insurance—it protects you from structural damage caused by natural disasters. Hazard insurance is determined by local risk factors such as fires, flooding and earthquakes, and it’s usually included in your homeowner’s insurance policy.

Mortgage insurance

Mortgage insurance protects your lender against loss if you default on the loan. This could cost up to 2% of your total loan amount per year if you didn’t make a down payment of at least 20%.

HOA/Co-op/Condo fees

These are monthly membership fees used to pay for improvements like landscaping and painting and for amenities like swimming pools and gyms. The fee varies dramatically based on the organization and where you live. Upscale condos and homes typically have higher fees and stricter rules than more modest digs.

Utilities

Electricity, gas, water, trash collection, recycling, internet, cable, and security monitoring are daily essentials that you pay monthly, and their costs vary depending on where you live. Bigger homes generally have higher utilities.

You better shop around!

You probably wouldn’t buy the first car you looked at, or the first pair of shoes you tried on, and so it is with the first lender you come across. Shopping around for the best mortgage takes time, but it’s time that can save you lots of money.

Mortgages don’t just come from banks—credit unions, brokers, and independent lenders also deal in mortgages. Know how much you can afford for your down payment, then choose a few institutions to approach for a loan. Ask for all of the costs involved in the loan, including all the stuff above. Compare the loans, and then approach the lender you like best. If you’re charming and savvy, you may be able to negotiate lower fees or better terms. Once you’re happy with what the lender is offering, get it in writing, or it’s not real!

Which is generally better, buying a home or renting? Millennials often don’t really get a choice. But let’s say you do, or are rising the economic ladder. Maybe you just want to know what your situation is affording you.

Of course, renting is appealing because it comes with fewer responsibilities, yet you also don’t get as much autonomy or privacy as with homeownership. There’s no easier way to make sense of buying versus renting than with good, old-fashioned pros and cons lists:

The PROS of RENTING vs. buying

You don’t have to pay property taxes or spring for homeowners insurance

When the furnace breaks down or the roof leaks, you don’t have pay for new ones

You’re free to move out with a 30-day notice

You don’t risk foreclosure if you lose your job or take a pay cut

A rental deposit is far less expensive than a downpayment on a home

You have fewer responsibilities, including upkeep

Utilities are generally less expensive in an apartment, and some are even included in the rent

The PROS of BUYING vs. renting

Mortgage payments build equity in the home

Homeowners often enjoy more tax deductions than renters

Homeownership offers a sense of stability and putting down roots

You can do whatever you want with your space

Pets are always allowed

Monthly payments end once your mortgage is paid off

You have an asset to borrow against if you want to make improvements

The CONS of RENTING vs. buying

Rent often increases, unless it’s fixed

Renting offers no tax benefits

Less stability—if the landlord sells and the new one wants you out, you have to go

You generally can’t customize your space—painting, knocking out walls, etc.

You have to rely on someone else to get things fixed or improved

Rent payments never end

Pets might not be allowed

The CONS of BUYING vs. renting

It costs a lot upfront to buy a house

It’s more expensive to maintain a home you own than a rental

You have to be more responsible—making sure the mortgage is on time, your sidewalks are shoveled, you don’t alienate your neighbors

Your home price might lose value, making it a poor investment

It requires a long-term commitment, which may be scary for some people

It’s far more difficult to move, since you have to sell your home first

You may be liable for injuries sustained on your property (hence the homeowner’s insurance)

If something happens and you can’t pay the mortgage, your bank may foreclose on you

Ideally, you need to have a buffer in savings in case something goes wrong

The Pros and Cons of Buying a Condo vs. Buying a House

Well, what about condos?

Houses and condos are like apples and oranges—sure, they’re both a place you live in, but other than, that they vary quite drastically. Your lifestyle might be better suited to a house over a condo, or vice versa. Don’t just look at prices when choosing which housing situation is best for you—here are some of the differences to take into consideration.

PROS of BUYING A CONDO vs. a house

A condo is generally less expensive per square foot than a house

Many condos have concierge services

Landscaping and exterior maintenance and repairs are covered by the homeowner’s association or HOA

Amenities like a gym, pool, or clubhouse are usually included

Homeowner’s insurance is less expensive

You’re part of a community

PROS of BUYING A HOUSE vs. a condo

A single-family residence offers more privacy than a condo

A house is easier to sell than a condo

You have direct, easy access to a private outdoor space to build a garden or install a pool

You have more creative freedom with your space

CONS of BUYING A CONDO vs. a house

You have less privacy since other people live on the other side of your walls

Potentially strict HOA can make it impossible to customize your condo

HOA fees can be expensive, and you pay them on top of the mortgage

Many condos don’t allow animals

You can’t DIY your outdoor space

CONS of BUYING A HOUSE vs. a condo

You’re responsible for handling the exterior issues, like painting, landscaping, maintenance

Utilities are more expensive

Potentially strict HOA may limit what you can do with your home

Rev-Up Your Credit Score, and Drive Down Your Interest Rate

Alright, but what about credit scores? Do they matter?

Without good credit, it’s going to be virtually impossible to score a low-interest rate on your home loan. Before you embark on a home-buying journey, it’s a good idea to check your credit score and pull your credit reports. If your credit reports have incorrect information, getting mistakes resolved before you apply for a loan can raise your score and net you a better rate.

“And while the average living wage is $68,808 a year, the average millennial makes just $35,592 a year…”

Three credit bureaus maintain files on how you handle credit, including whether you pay bills on time, skip credit card payments, or have items in collection. Different lenders have different criteria for various interest rates, but even a few points on your credit score can mean the difference between half a percentage point—and thus dramatically affect your monthly payments.

Many lenders use the Fair Isaac Corp. (FICO) model for ranking your credit score. This system grades you on a scale of 300 to 850 points, with 800 points or more indicating exceptional credit and under 579 points indicating poor credit. It’s not super easy to increase your credit score—it can take a little time, but the time is well worth it if it means a lower interest rate on your loan.

If you’re worried about your credit, here’s what you can do

Find your current credit score

First, check out your current credit score so you know what you’re dealing with. Order your credit report, which will give you information on which factors are most heavily influencing your score, such as late payments, credit-to-debt ratio, and items in collections.

Focus on virtually nothing else but paying off your debts

Make a budget plan to pay off any outstanding debts you have. Pay off the most expensive debts first, and work your way down the line. Try to pay more than the minimum balance on loans and credit cards each month, and utilize low-interest, balance transfer credit cards to keep the interest low.

Make all your bills scheduled to be automatic

Everyone forgets to pay a bill now and then, but chronic lateness has a negative impact on your credit score. This goes for all of your bills, including utilities, credit cards, and loans. Set up automatic payments for your bills, or set calendar reminders to help you pay on time.

Maintain good credit card debt-to-limit ratios

Credit card companies look at your credit utilization ratio to see how well you manage credit. This is calculated by taking the total amount of all of your credit card balances and dividing that amount by your total credit limit. Keeping your credit utilization ratio low shows lenders that you’re good at managing credit.

Don’t apply for new credit accounts unless you absolutely must

As you’re remedying your old debt, try not to rack up any new debt. Avoid opening up more credit accounts unless it’s absolutely necessary. The more credit accounts you have, or the more you apply for new accounts, the riskier you appear to be.

Keep unused credit cards open

It sounds logical to close your unused credit accounts, but doing so actually increases your credit utilization ratio and lowers your credit score. Unless the unused accounts are charging you fees, keep them open.

Check your credit report at least once a year

Once you’ve got your credit score under control, make sure to check it at least once a year, and report any inaccuracies to the appropriate bureau.

See prices for movers by the hour – instantly.

Read real customer reviews.

Easily book your help online.

How to Save Money for a Down Payment Without “Giving Up Your Daily Latte”

You probably love it when people tell you that if you’d just quit your daily Americano or avocado toast habit, you’d be able to afford a house, but you don’t have to listen to them. With a little creativity, you can save money without giving up your favorite creature comforts.

First, set a goal. Figure out roughly how much you’ll probably spend on a house, then figure out how much a 20% down payment will be. If that amount makes you spit out your coffee, try 10%. But don’t go any lower than that. Then, open a savings account if you don’t already have one, and start socking away money as you can.

Here are a few hot tips to help you reach your goal faster.

Treat your savings like a bill

Instead of looking at your savings like an optional expense that you can put off until next month, think of it as a fixed cost that you must pay, just like your electricity and phone bills. Have the money deducted from your paycheck and sent directly to savings so it never crosses your path.

Cut recurring expenses from your budget

Look at your spending habits, and decide where you’re able to cut down. Can you cancel your $100-a-month gym membership for a few months and hit the running trail instead? Eat or drink at home most of the time instead of ordering in or going out? Pare down your digital subscriptions to just the essentials? A little here and a little there will add up faster than you think.

Find a side hustle

Make some extra scratch each month with a second job. Rideshare services or food and grocery delivery are great options for a little extra cash if you have a reliable car. Bartend one night a week at your local dive bar, or tutor online.

Focus on your high-interest debt

Start hacking away at your credit card or loan with the highest interest rate. After you’ve paid off the balance, move on to the next. Transfer your high-interest rate balances to your card with the lowest interest rate.

Try These Sweet Programs for First-time Home Buyers

First-time buyers may be eligible for special grants and zero-interest loans through various state and local programs. Requirements for each program vary, so check with your state’s housing finance agency or the organization providing the loans to see what you’ll need to do. These are some of the loans available to first-time home buyers.

FHA loan

FHA loans are insured by the Federal Housing Administration and are for low-to-moderate-income buyers – they generally have lower credit score and down payment requirements than other loans.

The US Department of Agriculture guarantees loans for some rural properties and offers up to 100% financing. These loans are for low-income folks who don’t qualify for traditional mortgages. USDA loans are low-interest and don’t require a down payment.

The Department of Veterans Affairs offers zero-down payment loans for veterans, military personnel, and their spouses. They have low-interest rates and don’t require a minimum credit score to qualify. These loans have the option of being used to refinance an existing mortgage.

These loans are offered by the Department of Housing and Urban Development (HUD) for firefighters, law enforcement officers, teachers, and emergency medical technicians. Those who qualify receive a 50% discount off the listed price for homes located in “revitalization areas.”

State and local first-time buyer programs and grants

States and cities provide down-payment and closing cost assistance through these programs and grants if you’re a first-time buyer. Look into your state’s housing authority program for more information on the type of assistance available to you.

This is a VA-backed program that provides Native American veterans and their spouses to buy, renovate, or build houses on federal trust land. There is no down payment and the closing costs are low.

While the average age of first-time homebuyers is rising, that doesn’t mean there’s no hope for young people to buy a house if they want to. If you’re thinking you’re about ready to put down some roots, maybe grow a garden, and stomp around all you want without disturbing your downstairs neighbors, start saving today, improve your credit score, and find yourself a little piece of the earth to call your very own.

The Important Things to Take Pictures of While Moving (and Why)

Getting ready for the big move? Don’t pack that camera away just yet!

Besides getting those great social media shots (“I’m driving a U-Haul, everybody get off the road!”), taking pictures before, during and after your move can help protect your stuff – not to mention your wallet.

The main reason for taking pictures when you move might be obvious, but it is worth iterating. No matter how skilled, experienced and careful your movers are, accidents do occasionally happen. And if you don’t prepare, you may not be properly reimbursed for damage that occurs.

So before your movers show up, go around and take pictures of anything and everything you deem valuable. This means furniture, electronics, breakables and anything else you think would be difficult and/or expensive to repair or replace. Then when your move is complete and you find that something has been damaged, you will have proof that the item was in fact damaged in transit.

This also means taking pictures of existing damage: a scratch on your kitchen table, a dent in your dryer, or a small crack in the corner of your mirror. Why? Because if you suddenly find a bigger scratch, a deeper dent or a longer crack, your movers can say “That was already there.” “Yes, but it’s much worse now!” you will cry. And you will lose.

Knowing all that, here are some crucial tips for everything you’ll especially need to take pictures of.

Take photos of your cleaned-out apartment.

Believe it or not, there are some crafty landlords out there who would love to pocket your security deposit. Taking pictures of your old place before you leave for good can help you defend yourself against false claims of damage. And if you did damage something? Take a picture of that too, so that same unscrupulous landlord can’t charge you hundreds of dollars for fixing a couple of nail holes.

Protip: Take pictures of the bathroom and the shower. Yours truly got nailed for leaving the toilet “a filthy disgusting mess” after moving out of his Boulder, CO apartment, even though it was sparkling and sterile when I locked the door for the last time. I don’t even want to know.

Likewise, take pictures of your new place.

Again, don’t just photograph any existing damage you may find. Photograph everything! Why? Because walls, doors and light fixtures (and door jambs and floors and ceilings) can suffer damage during the move-in process. Your movers might be a great bunch of professionals, but you probably won’t want to have to pay for the gash they accidentally put in the kitchen floor.

Protip: Also take pictures of your rental truck! Get shots of any existing damage, inside and out, as well as the general condition of the interior of the cab and the back where all your stuff will be going – especially if these areas are less than pristine.

Take a picture of the back of your TV, for reference.

You know all those dusty wires back there? The ones to your surround sound system and your Blu-Ray player and your four different gaming consoles? It’s all going to have to be disconnected (and, probably, untangled). Having a photo of which wires go where can save a lot of time and aggravation when you are setting up your system at your new home.

Protip: Snapping a pic of the make, model and serial number of each of your electronic components can be a huge help in case you have to track something down – or, if something goes missing, to confirm that component’s age and value.

Take pictures of large, especially valuable or just unusual items.

This isn’t to highlight damage, but it’s simply a good idea to have pictures of things, from furniture to expensive décor to items that we’d rather not have to try to describe. Because if something goes missing, a picture helps A LOT in finding it. (Use your inventory sheets, people!)

True Story: A week or so after delivering a long-distance shipment we’d taken into our warehouse, I got a call from the customer. “I’m missing a chair,” she told me.

This was not very helpful.

We had literally hundreds of chairs on the 30-foot-high racks in our warehouse. Knowing that this chair was upholstered with a flowery fabric was only slightly better, and as the woman lived up in the mountains two hours away. She wasn’t about to come down and help me find the right one. “Let me fax you a picture of the chair,” she said. (Yes, this was a few years ago.) And even though the picture was black and white and a little blurry, I recognized it right away, saving me hours of searching during the already-hectic summer season and saving the customer from days, if not weeks, of inconvenience and uncertainty. (Not to mention a two-hour drive to our warehouse.)

Take photos of the water, electricity, and gas meters.

Do this both at your old place before you leave, then at your new one before you move in. Why? To protect against being charged wrongly for utilities. Not that the utility companies are out to scam you, but it’s quite common for them to charge based on usage estimates (which saves time and money on meter readers). If their baseline reading is off, then so is your estimated usage. There may also be a lag – or an overlap! – between customer accounts. Bottom line is, there are plenty of ways you can end up being charged for another resident’s utility usage. Taking photos of your meters can help immensely if such a situation comes your way.

Take a video of your electronics in action.

On their inventory sheets, movers describe anything electric, electronic or mechanical using the acronym “MCU” – mechanical condition unknown. This means they don’t know if something works. Which also means you can’t prove something was rendered inoperable during your move. Without proof, it’ll be difficult to get reimbursed for the flat screen that has suddenly gone to plasma heaven.

To guard against this, videotape your TV, stereo, air hockey table, pinball machine, lava lamp, or whatever to show that these things were indeed working properly before the movers showed up.

And ALWAYS timestamp your photos!

Imagine having pictures showing that you left your old place in perfect condition, but then having your old landlord claim that you took them before you did the damage he is trying to charge you for. Or owning a picture of the damage the movers did to your new place, only to have them say “No, that was like that before we showed up.”

How do you answer that?

There are a few ways.

Set your camera so the time and date show up on your photos.

Email your photos to yourself as soon as you take them.

Make sure your time and date is correct on your phone’s camera roll.

Even print out the photos you take and snail-mail them to yourself.

Protip: It may be easy for someone to claim that you simply changed the time/date setting on your camera before you snapped those incriminatory photos. So keep them on your memory card, sandwiched in between other pictures you took along the moving process – or even in between photos from before and after the process – to prove your timeline if need be. Most people are reasonable.

Are we being too cautious?

After all, the majority of moves – and the vast majority of HireAHelper moves – are completed without a hitch. But remember: accidents happen. Taking pictures can save you a ton of time and aggravation – not to mention a bit of cash – if something does go wrong.

×

I'm Moving

Moving? Thinking about moving? Whether your move is off in the distance or you already have one foot out the door, you'll learn about everything you should expect through our useful how-to's, cool articles and much more. It's all specially curated for you in our "I'm Moving" section.

For rookies or veterans alike, our "I'm a Mover" section is filled with extensive industry news, crucial protips and in-depth guides written by industry professionals. Sharing our decade of moving knowledge is just one way we help keep our professional movers at the top of their game.

Talking about money can be fraught for me, which I counter by talking about it pretty much all the time to build up my resistance. One area where I still struggle, though, is in

Talking about money can be fraught for me, which I counter by talking about it pretty much all the time to build up my resistance. One area where I still struggle, though, is in  Really quickly before I dive in, I want to note a couple things.

Really quickly before I dive in, I want to note a couple things.